Fleurets director and head of agency Simon Hall explains: "2015 will be seen as the point where the economic recovery started to reach the pub property market in all regions of England and Wales.

"The effect is, however, not consistent for all locations, tenures or styles of operation. From continued strong growth of rents and capital values in central London to the early stages of increased deal activity in many northern towns, the market is clearly moving.

"Merger and acquisition activity is very firmly back on the agenda with several tenanted and managed package deals completed in the past 12 months. With an abundance of private equity funds eager to invest in our asset-backed, high cash flow sector, a lot more is sure to follow. Pending legislation may slow short-term activity but whichever way the Market Rent Option (MRO) falls, deals are likely to follow."

But what does all this mean for YOU? Well, regardless of whether this is the year you finally cash out on your asset, are looking to grow your portfolio or simply interested to know what your property is worth, there may be a glimpse of some smoother waters ahead aboard the good ship Publican.

Here are our top ten findings from the report:

1) Economic recovery changing market dynamics

The underlying economic recovery and growing consumer confidence have stimulated sales growth. This improved trade performance has led to a change in market dynamics from being dominated by discount deals and bargain hunters to one where owners are holding more of the cards and buyers are fighting for the best of what’s around.

2) Growth of managed house operators

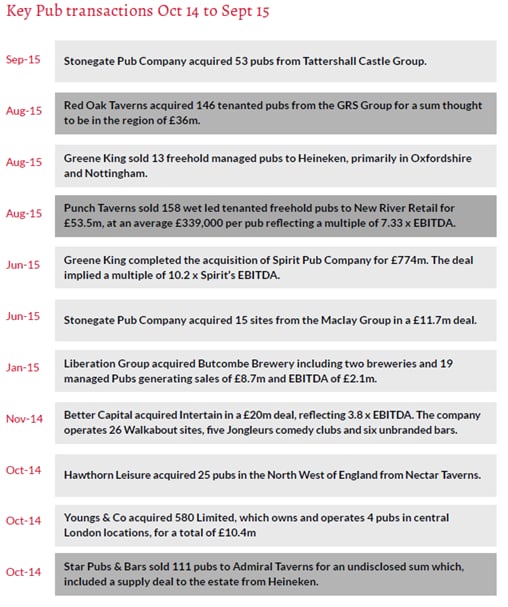

Managed house operators continue to grow their market share, either by new build (Marstons), individual acquisitions (JDW, Amber Taverns etc), or by group deals (Greene King with Spirit and Stonegate with TCG). Much of the focus is on managed food-led operations as this is a market in growth.

Fleurets anticipates the increase in merger and acquisition activity seen last year will continue, possibly accelerated following the MRO legislation.

3) Secondary regional towns tempting operators

Increasing prices in London are leading to many operators seeking better returns on their investments in regional centres. This is evident in cities such as Birmingham, Bristol and Leeds. In some of these regional cities, high levels of city centre activity is starting to tempt some operators to consider the secondary regional towns.

Freehold

4) Average freehold sale price up 5.5%

An increased demand paired with reduced supply has led to increased pub values in virtually all areas. As a result of this, the freehouse market is once again coming to life after several years of stagnation with sellers choosing to place their businesses on the market.

Despite a reduction in the volume of high-value London sales, the southern regions outside London saw an increase in average sale price of 3%. The south sold twice as many freehold freehouses as the north.

5) 23% decrease in freehold sales volume

One of the biggest factors affecting the pub market has been the continued reduction in the supply of bottom end freehold pubs. In 2014, Fleurets reported volumes in this category had fallen 25% and this was repeated in 2015 with a 23% decline. This was most acute in the south, which was down 38% in volume, compared with the north which was down 12%.

The reason for this would appear to be the number of pubco operators retaining bottom-end sites for development, often seeking to carry out developments themselves or in joint ventures to extract greater value. This would indicate the end of the mass disposal of tenanted pubs.

Fleurets predicts that sales going forward will reflect commercial estate management decisions involving the practice of "churning" underperforming properties to enable reinvestment. The average sale price of individual bottom end pubs is expected to increase as part of this.

6) Freehouse sales on the rise

At the other end of the freehold market, private owners of operational and viable pub businesses are being encouraged to test the market as demand levels increase. The second half of the year saw 35% more sales concluded across all regions compared with the first half of the year.

Leasehold

7) 46% increase in volume of leasehold deals

The most significant feature of the Fleurets statistics on leasehold pub transactions is that the volume of deals increased significantly, up 46% on 2014, reflected evenly in the north and the south. The increase in the volume of assignments and particularly free-of-tie leasehold transactions has provided greater diversification of the market and wider choice for operators of all varieties.

8) Increase in free-of-tie assignments

The growth of free-of-tie lettings and assignments is partly a result of the huge number of freehold pubco sales over the past seven years, swelling the privately-owned freehouse market. Purchasers of those freeholds who bought to let are now seeing the leases being assigned. Some purchasers who bought to occupy are now seeking to lease out their pubs, rather than sell or continue operating themselves.

9) Twice as many leasehold deals in the south

The average sale price of leaseholds is down 5% nationally, mainly as a result of the lower quality and geographical spread of deals. However, the average sale price in the north was up 27% due to a number of high value deals in the Midlands with a decrease of 13% seen in the south, largely as a result of a higher proportion of lower value letting transactions in the West Country.

Sale prices have ranged from "nil premium" with incentives to £700,000, with the highest number of six-figure premiums not surprisingly being achieved in London which accounted for 42% of leasehold transactions. Average sale price as a multiple of Free Maintainable Trade (FMT) remained broadly the same as last year at 0.13, split 0.10 in the north and 0.14 in the south. However, the average FMT was up 2.4% to £385,000.

10) Danger for tied licensees?

With the number of pub properties sold for alternative use on the rise again, the ACV debate rumbling on and MRO uncertainty casting a long shadow over positive signs of life in the pub property market, no doubt there is still some stormy weather out there.

Most worryingly for tied licensees, the growth in size of corporate deals may once again raise the question of who will truly benefit from the change in the market's fortune.

Though the number of significant corporate deals which took place last year was similar in number to 2014, the increase in scale saw almost twice the number of transactions and at nearly twice the total price.

The most significant group transactions in the 12 months to September 2015 (shown below) accounted for almost £1bn and involved 1,770 pubs.

Want to view the full report? Click here.