The rise of the ‘Netflix and chill generation’ means Britain’s pub haemorrhage, kicked off by the 2007 smoking ban, could be about to shift to another sector after a decade of adversity that has forever changed the face of the trade.

Casual-dining crisis

Key factors that have led to a spate of closures in the casual-dining sector:

- Over-inflated premiums paid to landlords on the granting of leases

- High annual rents

- Escalating business rates

- A rising cost base, particularly around food

- Increasing staff pay

- Too many competitors in a saturated market

- Squeezed consumer spending

- Falling numbers of diners

- Complacent offerings

For many, it will be refreshing to see the casual-dining chains that replaced their businesses finally come under strain. Though, for some, basking in the failures of competitors may be cathartic for a short while, it is perhaps more productive to explore what went wrong and what we can learn.

Despite being just three months into 2018, the landscape of the hospitality trade has dramatically changed, with several casual-dining chains – only 10 years ago growing business champions – failing or taking hits to their estates.

Celebrity chef Jamie Oliver’s Italian restaurant concept topped the news agenda when, in January, it was decided 12 of 37 sites would close due to financial issues. The late Antonio Carluccio’s restaurant legacy is the latest to come under pressure, after restructuring experts were brought in this month to advise on the future of the 102-site business.

Within Italian dining, pizza and pasta chain Prezzo is set to face the biggest losses, with up to 100 of its sites earmarked for closure. Adding insult to injury, fellow Italian brand My Restaurant – from lightweight celebrity chef Gino D’Acampo – announced it would, by 2019, add at least five new outlets to the existing eight.

Italian eateries are not the only concepts to struggle, however. Gourmet pie and mash group Square Pie announced the closure of its five sites after falling into administration last month and, in January, burger chain Byron said it would close 20 venues in the UK. Not to mention the other chains that have gone before them.

But a shift in the hospitality ecosystem, especially one that flies in the face of the modern ‘norm’ of constantly retrenching numbers, leaves the pub sector’s future just a little bit rosier. Last weekend (4 March) The Sunday Times claimed casual-dining segment disturbances – such as restaurant closures – were symptomatic of a saturated dining-out market, and were leading to a rise in wet-led pubs.

The number of restaurant closures seem high so far this year, but new openings still exceed those of pubs and bars. According to CGA data, for the five years to December 2017, the UK had 50,666 pubs and bars, 5,849 fewer than in 2012, while there were 27,312 restaurants – up 3,908 for the same period.

In 2016, the number of pub and bar openings slightly outweighed restaurants for the first time by 22, which was also the first year for the five-year period that restaurant numbers saw an overall decline, down by 387.

In the past three years, pub openings have risen by 828 to 1,695, meanwhile, for the same period, restaurant openings have increased by 633 to 1,961.

During the dark decade that followed the smoking ban, and the financial crash of 2008, pubs diversified into food to stay afloat. At the same time, the casual-dining sector hit a major growth spurt and flooded the UK with dozens of dining experiences. As a result, the market is saturated with food offers and struggling to attract promiscuous customers – who now have too many options – through the door.

“The pub, on the other hand, has seen its fortunes begin to turn, with like-for-like sales in the drinks-led managed market up 1.6% and total sales up 4.3%,” says CGA group CEO Phil Tate. “This is considerably outperforming the restaurant and pub food markets, with consumers returning to the pub [to drink] and business leaders of wet-led operations having a much more optimistic view of the future,” he adds.

Days of the smoking ban

While diversifying into food, a prescribed antidote to the sombre days of the smoking ban, which aimed at attracting diners and families, pubs maintained an unrivalled drinks offer and continued to welcome punters at the bar. At the same time, casual-dining chains, often with a cookie-cutter strategy, moved into the same space, but left little room for the drinker. Now, according to MCA data, fewer consumers are eating out, undeniably leaving a large market with significant choice but short on visitors.

“Business leaders in the sector today tell us that this market is becoming saturated and over-supply is a real fear for the year ahead,” Tate adds. “This is coupled with restaurant like-for-like sales growth of just 0.3%, considerably behind inflation, and a rising cost base, particularly around food and it is the effect of these pressures that are causing the high-profile closures in today’s market.

“Over the past 10 years it is fair to say the pub market has had a tough time, with the net rate of pub closures hitting 52 pubs a per week in 2009,” explains Tate. “Although the stock of Britain’s pubs has continued to reduce, albeit [now] at a slower rate, those that remain have adapted to meet changing consumer needs.” Indeed, CGA’s figures put pub closures in 2017 at around 34 a week, while the Campaign For Real Ale (CAMRA) claims that figure is now more like 18 a week.

In the past decade, pubs have adapted to challenges and brewed new concepts, yet casual-dining entrants have survived alone on the excitement of being new and different, leaving them with little need to regularly, if at all, change their models.

Individuality is a key unique selling point for the pub, says Star Pubs & bars operations director Tim Galligan. "Leased pubs are better placed than branded casual dining outlets as people like the individualism of these owner-run businesses. As well as distinct menus, they have more to offer and more to sustain them, such as a wide portfolio of quality drinks brands, coffee and activities.

"The closure of casual dining branded restaurants reduces competition on the high street, providing dynamic, invested, well-run pubs with an opportunity to increase trade."

The owner of award-winning seven-site-strong pubco Cheshire Cat Pubs & Bars, Tim Bird, argues that the likes of Jamie’s Italian quickly lost sight of what they set out to achieve. “If you put your name to something, you have to live and breathe it 24/7,” says Bird. “I remember taking my daughter to Jamie’s Italian for her 18th birthday, shortly after the Oxford Street restaurant opened.

“I liked it; the staff, the atmosphere and the fit-out all made it stand out in the ‘pseudo-Italian’ restaurant sector and above all it was Jamie Oliver’s place. It was claimed each Jamie’s raked in £75,000 a week and it took the market by storm. But it grew too quickly and lost its uniqueness and individuality.”

Jamie Oliver Restaurant Group CEO Jon Knight admitted at the Casual Dining Show in London last month there had been little brand innovation since launch, and the company had become “complacent”.

He added: “As a business, we lost our way, we hadn’t acknowledged how much the UK high street had changed over the past 10 years. Change wasn’t actioned quickly enough and the business became a little complacent in several key areas.”

That still leaves pubs, with an increased food offer and in an overcrowded market, questioning whether there is room for survival and if they should begin to focus more on drink. There is not, however, a simple yes or no answer.

In the 12 months to September, there was a small 0.9% decline in food pubs, which had risen by 5.3% to 18,000 sites in the five years to 2017, according to CGA’s 10th Market Growth Monitor report. The number of drink-led pubs dipped by 2.3% for the 12 months to September 2017 and by 18.3% for the past five years.

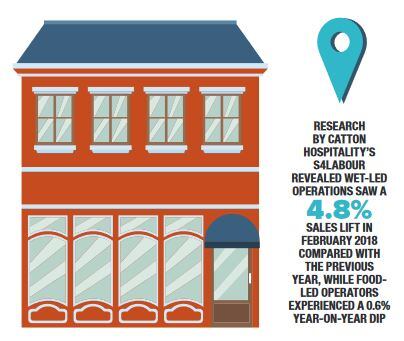

However, research by Catton Hospitality’s S4Labour revealed wet-led operations saw a 4.8% sales lift in February 2018 compared with the previous year, while food-led operators experienced a 0.6% year-on-year dip.

“Drinking pubs and bars can still do very well if they provide a distinctive offer that responds to the demand for on-trend drinks like craft beer and gin, especially in London and other big cities,” says the report.

Flexing more into drinks

City centre pubs are, according to the report, capable of flexing more into drinks because they have a deeper pool of consumers to target, but quieter locations, such as rural sites, must continue to maintain a mixed offer if there isn’t enough take up of drinks.

Some pubcos can sustain a business model based on selling more drinks than food. This includes London-based City Pub Company, which sees the majority of its sales come from beers, wines and spirits. It is a similar story for brewpub company Brewhouse & Kitchen, which, as well as having a good proportion of food sales, takes most of its money across its 11 sites from wet trade.

Some operators and so-called ‘trade experts’ scoffed at us for bringing back and developing the brewpub model and trying to scale up the offer, but the conditions are now perfect for brewpubs

Kris Gumbrell – Brewhouse and Kitchen

CEO Kris Gumbrell says: “Some operators and so-called ‘trade experts’ scoffed at us for bringing back and developing the brewpub model and trying to scale up the offer, but the conditions are now perfect for brewpubs to make a marked comeback. We operate in a climate where craft beer is driving the market, as the guest is clamouring for a unique and authentic experience.”

For Bird, despite the rumblings in casual dining, nothing has changed when it comes to being a successful hospitality business – be it pubs or restaurants. “The best will survive and the inconsistent will struggle,” he says. “There are a lot of poor pubs out there. The easy bit is getting a pub, but the hard bit is turning it into an institution, a place that over many years can be relied upon.”

One thing pubs can rely on, according to Bird, is their unique place in British society. “We [pubs] have the history, authenticity and tradition behind us,” he says. “We are woven into the fabric of our communities and a real pub will live on as long as we don’t change it into a branded casual-dining restaurant. Pub values are intrinsic to the pub’s survival.”

Looking into the current hospitality disturbances has not revealed a finite solution to the current issues, other than practising what continues to make a business successful – staying interesting, offering great service and ensuring what you offer stands out and deliver the best.

However, one thing that can be agreed on is that factors outside of a business’s control were a major contributing factor to recent casual-dining venue closures. Peter Wells, commercial director of brewer and pubco Charles Wells, points out the familiar financial burdens the likes of Jamie’s Italian will have faced.

“The biggest issues with the sites – and I look on from the outside – is the amount they pay in business rates and rents which is likely to cripple any business if they can’t break even on all of the overheads,” he says.

Such overheads, which also include staff pay and utilities, are a well-documented problem for pubs too. “The cost pressure on pubs is acute and increasing,” says British Beer & Pub Association chief executive Brigid Simmonds. “Of course, business rates remain an ever-present threat, but other regulatory costs like beer duty, auto-enrolment for pensions and, of course, the national minimum wage all add to the pressure.”

These outgoings contribute to the “perfect storm of costs”, UKHospitality chief executive Kate Nicholls warns. “Pubs have innovated and worked very hard to attract customers in the face of economic uncertainty and barriers to growth,” she says.

“But pubs face the same burdens and obstacles as casual-dining brands and restaurants, such as property taxes and rent rises, rising employment costs, a weakened currency and cost inflation, while uncertainty regarding Brexit has hit businesses right across the hospitality sector.”

We are left with a pub trade that continues to lose venues on a daily basis, but now giant ‘trendy’ corporations are involved in the struggle, perhaps the taxes and crippling business rates endured by the hospitality sector will be taken more seriously by Government.