Gas and electricity prices are closely correlated as around 40% of our electricity is generated from gas.

Current costs

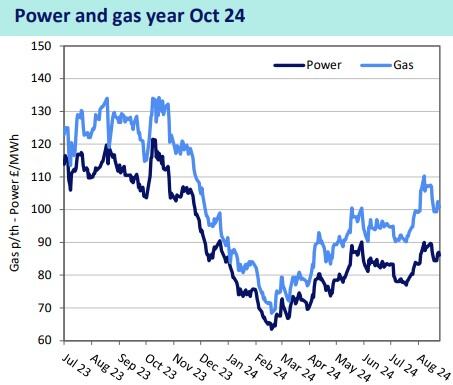

Energy costs have increased from the low point in February.

The table suggests the non-commodity element, including supplier margins and other costs, for electricity, is around 17p and 3p for gas. If commodity costs rise, I expect non-commodity costs will rise too, due to suppliers adding risk.

Several factors continue to influence volatility and cost movements:

Military conflict

Ukraine's incursion into Russia was unexpected and its ongoing expansion provoked increasing attacks on its energy network. Russia continues to flow gas through Ukraine to central and eastern European countries. This may change if Ukraine is permitted to use longer-range Western-made weapons.

The Middle East appears to be slowly escalating. The humanitarian crisis deepens. Both sides are using greater military force. International diplomacy shows no progress.

The Iranian-backed Houthis continue to attack shipping. The stricken Greek oil tanker, Sounion, sits abandoned by its crew and its cargo of 1 million barrels of oil continues to present a risk of an environmental disaster.

Developments in both conflicts are unknown, as is their impact on global gas and oil supplies. As we enter the colder months, we can expect heightened reactions to future adverse events.

Weather

Severe heatwaves continue in Asia, maintain increased LNG demand for generation for air conditioning.

The depths and duration of any cold snap can’t be predicted presently. In cold weather gas reserves are depleted more quickly than they can be replaced. A prolonged cold snap or significant reduction in supplies will reduce gas reserves driving up costs.

Supply interruptions

Unexpected losses in gas & LNG production arise from a range of sources - extreme weather events, industrial action, engineering & maintenance scheduling or delays in transportation.

Extreme weather and maintenance outages are less likely in the winter. The main risk would be from political or military events.

Future costs

Prices are unlikely to return to 2022 levels as:

- There is more gas storage capacity.

- Demand is lower and we know how demand can be managed.

- More renewables are available for generation.

Businesses with contracts ending in the next 6 months, need to carefully consider when to fix their next contract. Those who can afford for prices to rise a few ppkW have the option to see where the market goes. However, if renewal quotes are around maximum budgets, it would be prudent to fix now.

Nationwide Energy can provide a consultation, a market review and bespoke prices. Contact us on 02476 328995 or at info@nationwide-energy.co.uk. Also, see here for a free guide to help your business.