The Beer Orders

Published at the end of 1989, the Beer Orders followed a Monopolies & Mergers Commission inquiry that found the industry was a ‘complex monopoly’ and, along with other measures, recommended brewery-tied estates should be capped at 2,000 pubs.

The legislation itself was a compromise. The Big Six were given two years to either sell, or were allowed to go free-of-tie, half the difference between the number of pubs they owned and the 2,000 threshold – which added up to 10,791 houses.

Pub tenants were brought under the protection of the Landlord & Tenant Act and those running Big Six pubs were given the right to stock a cask ‘guest beer’ from outside the tie. Restrictions were placed on loan ties, too.

There it is. Statutory instrument no. 2390, ‘The Supply of Beer (Tied estate) Order’ looks harmless enough, doesn’t it? But this piece of paper was destined to kick the UK’s pub and brewing industry into the air, watch it flail around, hit the ground a different animal and continue to chase around in a frenzy.

Thirty years on, we’re still grappling with the challenges. The Beer Orders, as the dry legislation was wetly abbreviated, changed the world of pubs and the people who work and drink in them and, even though they were revoked in 2003, we can see its impact rippling through the trade today.

Children of the Beer Orders

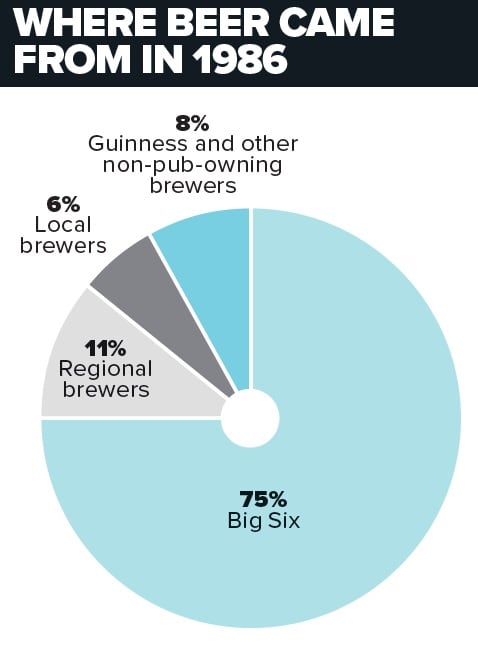

Before the Beer Orders

The UK brewing industry was dominated by the ‘Big Six’: Bass, Grand Met, Courage, Whitbread, Allied and Scottish & Newcastle. Between them, they owned 34,000 pubs – 45% of the total in the UK – and supplied 75% of the beer going to the on-trade, where 84% of beer was drunk.

Two thirds of their pubs were run as traditional tenancies, typically three-year agreements – fully tied for beer and often other products. The rest were directly managed.

They also controlled the market through loan ties to freehold pubs – lending them money in return for stocking their beer. Taking into consideration the tied estates of smaller, regional brewers, the Monopolies & Mergers Commission estimated 90% of pubs were restricted on choice.

Brewery profits were increasing by an average 15% a year – despite the Big Six running at only 75% of capacity. Between 1973 and 1986, the price of a pint rose from 13p to 84p, a hike of 20% above inflation.

Let’s go back to the beginning. By the late 1980s, the vertical integration of brewing and pubs – the tie – had been investigated by competition authorities several times with little result. Of all governments, it was Margaret Thatcher’s, that tribune of free enterprise, that eventually acted.

When trade and industry secretary Lord Young said he was ‘minded’ to accept the recommendations of the Monopolies & Mergers Commission report of February 1989, British brewing was shocked and bewildered that an old ally had, apparently, turned on them.

The Brewers Society, now the British Beer & Pub Association, described the plans as a “charter for chaos”.

Such a drastic state intervention may still have been averted through negotiation, but mistakes were made. Sir Peter Luff, who worked for Lord Young at the time, revealed in an interview with The Morning Advertiser earlier this year that a letter from the industry requesting dialogue with the minister failed to reach its destination.

“The one thing we got wrong was the Beer Orders,” said Luff who, as chair of the Pub Governing Body, is still trying to sort out some of the fallout.

Yet, two of the larger regional brewers falling below the proposed 2,000-pub cap on tied estates welcomed the Orders.

Both Greene King and Wolverhampton & Dudley looked forward to “tremendous opportunities”.

As far as the drinking population was concerned, the government simply promised that the Beer Orders, by increasing competition, would bring cheaper beer.

But, which is clear now, that didn’t happen. The price of a pint in the pub continued to rise above inflation, and the European Commission found the average differential tenants were paying per barrel above free market prices rose from £19 in 1991 to £48 in 1997.

And while drinkers and tenants continued to grumble into their beer, massive structural changes were triggered at industry level.

The ‘Big Six’ (see Before e Beer Orders) complied with the Orders and went further, by 1992 shedding some 12,500 pubs. At least half were bought by independent pubcos set up to take advantage of the sell-off, seeking to make a profit from both rent on the property and the margin they could charge licensees on beer, known as the ‘wet rent’.

Forming a powerful force

Leading pub owners before and after the Beer Orders

1988

- Bass – 7,190

- Allied – 6,678

- Whitbread – 6,483

- Grand Met – 6,419

- Courage – 5,002

- Scottish & Newcastle – 2,287

1992

- Bass – 4,595

- Inntrepreneur – 4,350

- Allied – 4,339

- Whitbread – 4,241

- Pubmaster – 2,026

- Scottish & Newcastle – 1,850

- Grand Met – 1,650

Pub estates in 2001

- Nomura (Inntrepreneur) – 6,000

- Punch Taverns – 5,100

- Enterprise Inns – 3,400

- Bass/Six Continents – 2,600

- Laurel (Whitbread) – 2,550

- Scottish & Newcastle – 2,500

- Pubmaster – 2,000

- Wolverhampton & Dudley – 1,800

- Greene King – 1,700

Meanwhile, the Beer Orders prompted the major brewers to make two other moves that were to have a lasting impact.

As local authorities looked to create a vibrant nightlife in town and city centres, brewers poured cash from the sales into managed estates to compete with high street operators like JD Wetherspoon, converting former banks and other prominent buildings into a new breed of super pub.

There were food-led concepts, too, as brewers embraced the vision they could be retailers and not just pub owners. Tony Thornton, in his book Brewers, Brands and the Pub in their Hands, lists 149 different retail pub brands that have come, and mostly gone.

Circuits of giant vertical-drinking venues lured thousands of young people out on a Friday and Saturday night, providing a media spectacle that would feed concerns about ‘binge-drinking’ and threaten the liberalising reforms of the 2003 Licensing Act.

Today’s late-night levy and the continuing controversies surrounding the drink question can be traced back to the Beer Orders.

As can a change in the very concept of what it means to be a publican.

To evade the Landlord & Tenant Act and to shift operation costs on to the licensee, the big brewers introduced long leases of, typically, 10 or 20 years that, unlike traditional tenancy agreements, obliged the publican to maintain the property and take more responsibility for the business.

In return, the lease was assignable, meaning that if a lessee was able to grow the business they could, in theory, sell it on at a profit. But, it wasn’t quite a new idea. Watneys’ brewer Grand Met had launched the Inntrepreneur 20-year agreement in 1988.

Still buying beer through the tie, and plunged into the recession of the early 1990s, many of these new lessees failed to realise their dream.

Then the licensee-entrepreneur changed the nature of the trade. Labour MP Stan Crowther, parliamentary advisor to tenants’ organisation the National Licensed Victuallers Association, estimated 40% of tenants left the industry rather than transfer to a long lease.

The pubcos, most of which had continued with the tenanted model, introduced leases, too. By 1994, there were more than 100 of them.

They had modest beginnings. Enterprise Inns, which was to end up the largest pub owner in the country, was launched with just 368 pubs from Bass.

But the drive to consolidate soon kicked in. Pubcos discovered securitisation, a way of borrowing money against future rents, fuelling a wave of acquisitions within the sector.

By 2001, the number of pubs held by brewers had fallen to 22.5% of the total. The government concluded the Beer Orders had done their job and revoked the legislation in 2003. Greene King took its estate beyond the 2,000 mark the following year, and Wolverhampton & Dudley, now Marston’s, was next.

One unintended impact of the Beer Orders was already promising trouble. Between 2001 and 2004, some 10,000 pubs changed hands in £4bn-worth of deals, a surge of consolidation that left Enterprise (now Ei Group) and Punch Taverns (now Punch), which joined the party by merging the Bass lease estate and 3,600 Allied pubs, with 17,400 pubs between them.

The ‘Big Two’ – Enterprise Inns and Punch Taverns – were bigger than the Six had been collectively.

Government scrutiny

The Beer Orders in numbers

- Barrel prices rose from £19 in 1991 to £48 in 1997

- Growth of Enterprise Inns from 3,400 in 2001 to 9,000 in 2004

- Growth of Punch Taverns from 5,100 in 2001 to 8,400 in 2004

- Between 1973 and 1996, the price of a pint rose from 13p to 84p – a hike of 20% above inflation

- Tony Thornton in his book Brewers, Brands and the Pub in their Hands, lists 149 different retail pub brands that have come and mostly gone

- In 2016 a statutory code was imposed on companies with more than 500 overseen by an adjudicator

- The big six complied with the Beer Orders and by 1992 they had shed some 12,500 pubs

- Enterprise Inns, destined to be the biggest pub owner, was launched with just 368 pubs from Bass in 1991

- Between 2001 and 2004, some 10,000 pubs changed hands in £4bn worth of deals

- By 2001 the number of pubs held by brewers had fallen to 22.5% of the total

Burdened by eye-watering levels of debt they struggled to give their pubs, and licensees, the investment they needed.

And with tenants increasingly squeezed by rising rents and the costs of the tie, the industry once again came under government scrutiny. So, a series of inquiries put pressure on pubcos to ensure their dealings with tenants and lessees were fair and transparent.

Pubcos responded to the crisis by shedding pubs and introducing a wider variety of agreements, including hybrid ‘managed tenancies’ that offered inexperienced licensees greater support, and free-of-tie deals to selected partners.

One positive result was the opportunity, in the past decade or so, for entrepreneurs to enter the industry and create a plethora of multiple operators that have played an important part in raising standards and generating innovation.

But the industry’s efforts were not enough to satisfy politicians and a militant tenants’ lobby. In 2016, a code was imposed on companies with over 500 pubs, overseen by an adjudicator.

The principle that a tied tenant should be no worse off than a free-of-tie tenant was enshrined in law and backed by the market-rent-only (MRO) option, giving licensees the right to negotiate a free-of-tie deal.

While controversy rumbles on over whether the code is working effectively, in the past couple of years the industry has continued to restructure in a sometimes dramatic fashion.

Punch Taverns was broken up with 1,900 of its houses going to Star Pubs & Bars, formerly Scottish & Newcastle and still brewery-owned, by global giant Heineken, leaving Punch with just 1,300.

Enterprise, having scaled back its estate to 4,000 and developed a substantial managed arm, was taken over this year by leading and growing high street operator Stonegate.

The years of crises have also seen pubs close at an alarming rate, not all down to the Beer Orders, of course, but they have played their part in the accelerated evolution of the industry.

One thing, at least, has not changed. Beer is as important to pubs as ever, and the tie is arguably making a comeback through an expanded Star Pubs & Bars, the growth in their estates that Greene King and Marston’s anticipated, and scores of new brewers opening pubs and taprooms.

One chapter in the Beer Orders story seems to be coming to an end. But a new one is, as ever, beginning, and the future is no more certain.