The Drinks List: Top Brands to Stock 2019

What a difference a year makes. When the hard facts on drinks trends and what people are really buying are laid before you, it puts into perspective what punters are actually drinking in outlets across the UK.

So many times this year we have heard that low and no alcohol is a rising trend. How many operators, though, truly believe that? Another frequent line is that premium is on the rise.

Again, where’s the proof? The same experts also say sugar-free and low-calorie drinks are becoming more important in the on-trade. But are they actually?

In the Drinks List this year, the truth about trends is exposed, with the facts spread out across the pages of this special issue, dedicated to showing operators what to stock in the coming months.

Data provided by CGA, which looks at the 12 months to 11 August 2018, shows the true picture. There is no ulterior motive, no outside input or editorial interpretation, just the facts, making the Drinks List a rare source of guidance.

“The 2018 Drinks List reflects a lot of the key trends that we are seeing in the market,” says CGA director of client services Jonathan Jones.

“Key categories such as lager, vodka and gin have a fairly even mix of standard and premium brands on their top sellers lists, which shows just how widespread premium drinks are in the market today and not just in top-end outlets.”

Within lager, the category boasting the bulk of on-trade sales, a big shift in consumer preference is clear.

Mainstream lagers

Mainstream lagers, for instance, have been in decline for some years. However, the haemorrhage appears to be clotting, as leading brews Carling and Foster’s show slower rates of volume decline, down 3.6% and 6.6% respectively. Marketing and brand refreshes could be accountable for the shift, as well as demand from consumers for trusted drinks.

Within the lager category, premium and world varieties are on the up. Peroni has put in an exceptional performance in the past 12 months, with both volume and value sales up 2.9% and 5.4% respectively.

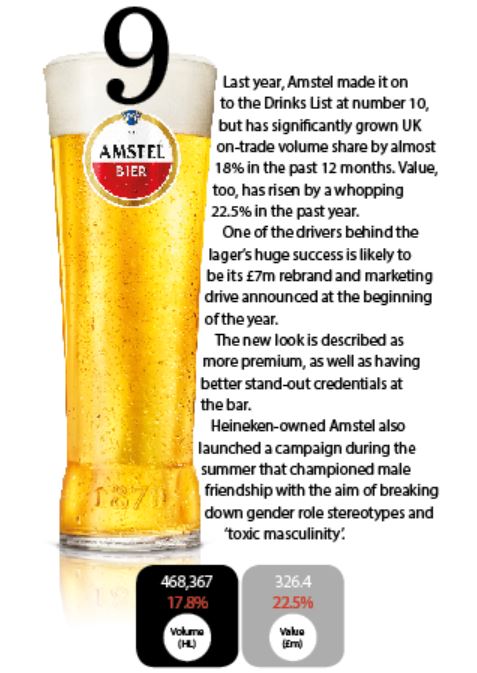

Amstel and San Miguel are also on the rise, with both volume and value sales up significantly, particularly Amstel, showing a 17.8% uptick in volume and 22.5% in value.

The trend for ‘healthier’ brews too can be seen in the list this year. Although brand owner Molson Coors wouldn’t promote Coors Light as a lower-calorie option, it is likely increased demand from consumers for beers lighter on the calories has played a role in a 17.9% increase in volume sales.

Bud Light, which does not appear among the top 10 lagers this year, has pushed the lower-calorie credentials of its lager hard in the past 12 months.

Owner AB InBev also relaunched light beer Michelob Ultra in the UK, indicating it sees more potential for sales within the segment.

Bud Light has made big gains in the off-trade, but doesn’t have such a presence in pubs.

However, it has increased on-trade volume sales from 41,000 hectolitres (hl) last year to 116,000 this year, making it one of the biggest winners in 2018.

Within the craft-beer space, which many may assume is a heavy volume category, the biggest selling BrewDog Punk IPA sells just a fraction of the most popular lager at 47,000hl (+47.6%) with a value of £42.5m (+44.7%).

Craft beer sales

Although craft is only a small chunk of the market – between 5% and 7% of total beer sales – the value percentage growth exceeds that of any other category.

Also, none of top-10 craft beer brands show value decline and, when compared with other categories, which all except gin show at least one product with value decline, shows the segment has legs for further growth in the year ahead.

No- and low-alcohol beer is also on the up. Although an extremely small category, there is year-on-year growth.

It is still led by Beck’s Blue, but new entrant Heineken 0.0 has put in a good performance since launching, growing volume sales to almost 7,000hl, yet still a fraction of Beck’s Blue’s near 20,000hl.

“Another shift we are seeing in consumer behaviour is towards health and wellness, one of the drivers of the continued growth of light beer, with the category now stocked in a quarter of all on-licensed premises and accounting for 9% of total lager volumes,” adds Jones.

‘Low and no’ is also having an impact within soft drinks, with volume sales of sugar-free products on the up, while full sugar drinks have shown a slight dip.

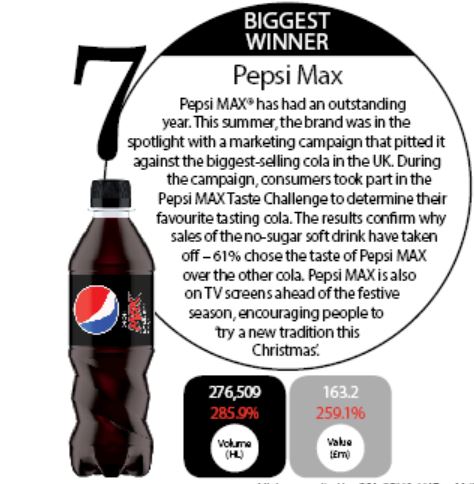

Coca-Cola Zero Sugar, Pepsi Max, Fever Tree Naturally Light Tonic Water, Britvic Low Calorie Tonic Water and Schweppes Slimline Tonic Water are all in growth.

It is also worth noting that Pepsi Max did not appear among the top 10 soft drinks last year, but ranks seventh this year.

If nothing else, this demonstrates consumers are becoming more health-conscious and aware of the calorie content of their drinks.

The sugar tax

Add the implementation of the sugar tax to the mix and there could be a time in the near future where sugar-free soft drinks will lead the way.

However, the big brands, such as Coca-Cola Classic and Fever Tree Tonic Water, still reign, which also suggests that consumers have a treat mindset when drinking in the on-trade.

“We see the health and wellness trend in soft drinks as well, with a low-sugar brand now occupying the number two slot and two zero sugar brands among the top sellers, when there weren’t any last year,” adds Jones.

“Sugar tax has driven changes to stocking in many outlets but there is a clear consumer demand for lower calorie drinks as well.”

Wine, meanwhile, has seen the biggest shift of new brands entering the list, as well as the most movement among remaining brands. Three new wines have entered the list this year, including two Proseccos and one rosé.

Jack Rabbit Chardonnay and Merlot have both risen three places, while Blossom Hill White has dropped four slots compared to last year.

All but two wines on the list have shed volume and value sales, with new entries Mionetto Il Prosecco and Bolla delle Venezie Pinot Grigio showing substantial growth.

Within spirits, vodka brand Smirnoff Red takes top spot, selling almost 1.2m nine-litre cases. Among the top 10 brands there is a mix of varieties, with no one spirit type dominating.

Only gin, Cognac and rum brands are in volume growth. Gordon’s gin, meanwhile, has moved into second place over Jägermeister from last year, a nod to gin’s popularity over the past year, particularly during the long hot summer, which sparked increased demand for gin and tonic.

Top 10 cider

This year’s list of top-10 cider brands remains much the same as last year. However, Strongbow Dark Fruit has strengthened its spot in second position, with potential to take the lead in the future, with volume sales at 519,417hl.

“The on-trade is key for driving trial on new products so it’s great to see some brands on the biggest growers list are completely new to market while others are relatively young brands within the top sellers of their categories,” continues Jones.

“There have been more than 4,000 new product launches in the past three years, so making the cut to build a successful brand can be tough.”

The ready-to-drink category’s line-up is the same as last year, but there is growth among the rankings.

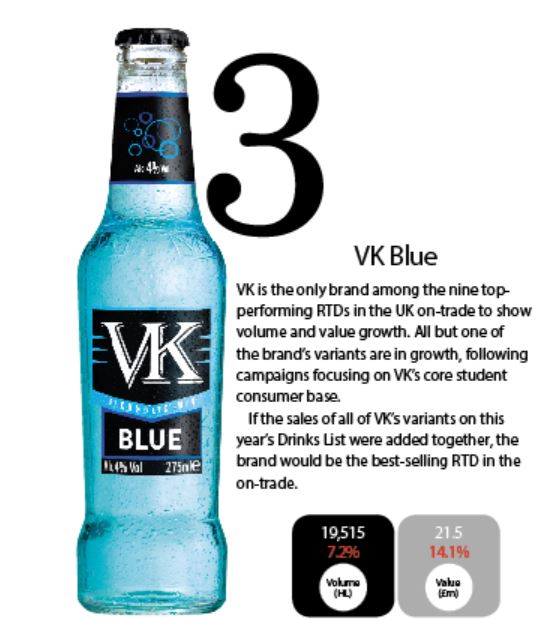

VK is the only brand to see both volume and value sales growth across all but one of its four variants on the list. Much of VK’s marketing activities over the past two years have focused on students.

When it comes to the question of the reality of drinks trends and whether or not the experts and analysts are right, this year’s Drinks List broadly backs what is being said.

Premium, including craft beer and world lagers, is on the up, consumers are looking to splash out a little more when drinking in the on-trade, and punters are becoming more health-conscious.

What is obvious, though, is the impact brand marketing can have on sales. Many products showing growth have either undergone a redesign or launched new campaigns.

When looking at drinks trends using the most popular brands, a real sense of what is happening at the bar can be attained.

- All data provided by CGA, which looks at the 12 months to 11 August 2018

Lager

Lager is an interesting category, with half of the top 12 brands showing fairly substantial growth. Those products in decline, meanwhile, are tipping only slightly into the red.

Brand | Volume (HL) | % +/- | Value (£m) | % +/- |

1) Carling | 3,064,216 | -3.6 | 1,706.5 | -1.9 |

2) Fosters | 1,922,906 | -6.6 | 1,116.1 | -3.8 |

3) Carlsberg | 1,036,724 | -13.1 | 558.5 | -12 |

4) Peroni | 757,018 | +2.9 | 721.1 | +5.4 |

5) Stella Artois | 672,943 | -3.7 | 445.9 | -2.5 |

6) Coors Light | 654,349 | +17.9 | 390.8 | +20.9 |

7) Tennents Lager | 540,625 | -1.5 | 303.6 | -0.1 |

8) San Miguel | 515,446 | +4.4 | 358.9 | +7.2 |

9) Amstel | 468,367 | +17.8 | 326.4 | +22.5 |

10) Kronenbourg 1664 | 366,757 | -11.0 | 247.1 | -8.1 |

Cask

Our national drink has, unfortunately, faced a series of sales dips in recent years. However, those in the segment remain optimistic about the brew’s future and rightly so, as cask has a lot to offer.

Brand | Volume (HL) | % +/- | Value (£m) | % +/- |

1) | 245,694 | +3.2 | 142.37 | +4.1 |

2) | 150,767 | -6.9 | 86.35 | -2.7 |

3) | 107,982 | -5.7 | 68.12 | -1.5 |

4) | 62,319 | -1.6 | 35.37 | -2.4 |

5) | 52,457 | -8.0 | 33.6 | -5.3 |

6) | 47,833 | +8.7 | 26.24 | +10.5 |

7) | 46,037 | -9.0 | 25.93 | -6.5 |

8) | 37,726 | +1.8 | 23.7 | +5.8 |

9) | 36,414 | N/A | 23.39 | N/A |

10) | 34,504 | +7.8 | 12.51 | +2.7 |

Craft beer

Although craft only makes up a small percentage of total beer sales, it has the loudest voice making it seem a bigger category than it actually is.

Brand | Volume (HL) | % +/- | Value (£m) | % +/- |

1) | 47,090 | +47.6 | 42.5 | +44.7 |

2) | 37,781 | +36.8 | 33 | +36.6 |

3) | 37,175 | -1.3 | 35.8 | +0.6 |

4) | 34,710 | +28 | 21 | +29.6 |

5) | 28,315 | +39.3 | 25.8 | +41.5 |

6) | 28,044 | +1.8 | 26.7 | +3.7 |

7) | 19,039 | +52.4 | 16.2 | +48.4 |

8) | 18,941 | +16.3 | 11.6 | +19.2 |

9) | 16,777 | +19.7 | 14.4 | +23.2 |

10) | 16,355 | +53.3 | 13.7 | +66.2 |

Low and no-alcohol beer

A rising star in the beer world, low- and no-alcohol beer is stepping up its sales volume and value performance, as drinking trends continue to change.

Brand | Volume (HL) | % +/- | Value (£m) | % +/- |

1) | 19,780 | +1.5 | 19.2 | +4.4 |

2) | 6,829 | +932.5 | 5.4 | +967 |

3) | 2,586 | +62.4 | 2.1 | +70.7 |

4) | 2,522 | +15.1 | 1.6 | +14.6 |

5) | 1,956 | -30.2 | 1.7 | -28.2 |

Cider

Cider sales are changing as more new product development drives excitement in the category – particularly around fruit-flavoured variants.

Brand | Volume (HL) | % +/- | Value (£m) | % +/- |

1) | 619,408 | -5.1 | 350.2 | -3.8 |

2) | 519,417 | +34.9 | 307 | +39.8 |

3) | 298,688 | +0.3 | 182 | +3.5 |

4) | 125,784 | -10.6 | 102.6 | -7.3 |

5) | 123,044 | -0.1 | 79 | +4 |

6) | 122,088 | -12.4 | 96.4 | -9.5 |

7) | 80,025 | +1.6 | 68.1 | +1.7 |

8) | 77,301 | -13.1 | 48.1 | -10 |

9) | 77,217 | +6.3 | 38.7 | +1.2 |

10) | 72,497 | -6.9 | 54.1 | -5.6 |

Spirits

A growing on-trade category, this offers operators investing in spirits significant financial gains, if they get it right.

Brand | Volume (9LC) | % +/- | Value (£m) | % +/- |

1) | 1,163,059 | -3 | 1,110 | -0.2 |

2) | 312,516 | +6.7 | 290.8 | +9.7 |

3) | 302,858 | -2 | 314 | +2.9 |

4) | 255,316 | -5.6 | 271 | -3.1 |

5) | 216,335 | +14.3 | 207 | +17.1 |

6) | 149,775 | -5.7 | 129 | -3.7 |

7) | 145,651 | -8.5 | 139 | -6.1 |

8) | 128,907 | +2.5 | 138 | +6.1 |

9) | 128,424 | -4.2 | 80 | -1.4 |

10) | 109,349 | +7.9 | 128 | +9.2 |

Vodka

The biggest spirits category by a mile, vodka remains the behemoth on any bar when it comes to mixed drinks sales. However, it has experienced its fair share of sales dips in recent years.

Brand | Volume (9LC) | % +/- | Value (£m) | % +/- |

1) | 1,163,059 | -3 | 1,110 | -0.2 |

2) | 97,086 | -3.4 | 116 | -1.1 |

3) | 94,603 | +35.5 | 105 | +37.5 |

4) | 58,946 | +111.6 | 79 | +105.8 |

5) | 46,571 | -2.5 | 67 | -1.3 |

Whiskies

Southern Comfort

Southern Comfort has been busy in recent years aligning itself with only the best bartenders in the world. Gone is the brand’s former ‘Soco’ whiskey and cola strap line, which has been replaced with a trendy and sleek approach to spirits and cocktail drinking.

With the new addition of Southern Comfort Black earlier this year, the brand hits all levels of price and taste on the bar, giving supplier Hi-Spirits the ammunition it needs to cater for a wide variety of business and consumer desires.

Southern Comfort has a revitalised 'The Spirit of New Orleans' branding which emphasises its roots in the United States’ cocktail capital and its whiskey credentials, as well as the accessibility and mixability of this iconic US brand.

Alongside Southern Comfort Original at 35% ABV, distributor Hi-Spirits has added Southern Comfort Black at 40% ABV and super premium Southern Comfort 100 Proof (50% ABV) to the range.

With more whiskey-forward blends that help recapture the 1874 original created by New Orleans bartender M.W. Heron, these additions are extending the brand’s consumer reach and helping ensure Southern Comfort’s place as a back bar essential.

The second largest spirits category in the UK on-trade, whisky is often and wrongly misconceived as a difficult and stubborn spirit.

It’s not though, and happens to be one of the most promising categories when it comes to customer satisfaction and drinks sales.

Brand | Volume (9LC) | % +/- | Value (£m) | % +/- |

1) | 255,316 | -5.6 | 271 | -3.1 |

2) | 149,775 | -5.7 | 128.9 | -3.7 |

3) | 108,754 | -10.3 | 98.3 | -8.8 |

4) | 54,188 | +7 | 58.4 | +10.2 |

5) | 51,303 | -11.6 | 52.7 | -8.5 |

6) | 35,984 | -5.6 | 46.1 | -3.0 |

7) | 27,081 | -7.3 | 17.7 | -8.8 |

8) | 20,563 | +2.5 | 27.9 | +8.3 |

9) | 14,511 | +4.6 | 18.8 | +8.9 |

10) | 11,843 | +29 | 14.8 | +36.6 |

Gin

The word on everyone’s lips is still gin. With new distillers and variants, innovation is driving the category.

Yet, just five brands take majority share, and a new pink gin is among them.

Brand | Volume (9LC) | % +/- | Value (£m) | % +/- |

1) | 312,516 | +6.7 | 290.8 | +9.7 |

2) Bombay Sapphire | 109,349 | +7.9 | 128 | +9.2 |

3) | 105,122 | N/A | 102.2 | N/A |

4) | 83,418 | +33.2 | 105.3 | +35.8 |

5) | 67,357 | +25.5 | 89.4 | 28.6 |

Rum

Arguably one of the easiest categories to trade up in, rum has long been predicted to be the next big spirit in the on-trade.

Brand | Volume (9LC) | % +/- | Value (£m) | % +/- |

1) | 216,335 | +14.3 | 206.9 | +17.1 |

2) | 145,651 | -8.5 | 139.1 | -6.1 |

3) | 49,341 | -0.2 | 46.5 | +2.8 |

4) | 28,613 | -5.6 | 32.2 | -1.1 |

5) | 25,013 | +45.8 | 30.6 | +49.7 |

6) | 22,301 | -1.2 | 26.9 | +1.8 |

7) | 21,294 | -0.3 | 26.1 | +1.2 |

8) | 15,410 | +6.8 | 24.8 | +8.7 |

9) | 10,191 | +42.9 | 9.6 | +39.1 |

10) | 9,547 | +7.4 | 12.7 | +12.5 |

Mixers

Where would we be without our mixers? Few of the spirits categories, particularly gin, would certainly not be experiencing current levels of growth.

Brand | Volume (HL) | % +/- | Value (£m) | % +/- |

1) | 92,788 | +55.6 | 96 | +50.7 |

2) | 90,679 | -5.3 | 83.9 | -5.3 |

3) | 58,345 | +12.2 | 53.4 | +12.4 |

4) | 42,574 | +7.4 | 38.5 | +2.4 |

5) | 40,062 | +148.3 | 40.9 | +141 |

Soft drinks

Despite the recent implementation of the sugar tax, the soft drinks category has maintained its position by using sugar-free variants to its advantage.

Brand | Volume (HL) | % +/- | Value (£m) | % +/- |

1) | 944,400 | -2.6 | 568.4 | +1.5 |

2) | 705,871 | -1.2 | 436.4 | +2.6 |

3) | 621,691 | -21.6 | 361.4 | -24.3 |

4) | 466,438 | -4.5 | 238.5 | -1.9 |

5) | 434,285 | -12.3 | 227.3 | -11.3 |

6) | 427,447 | -7 | 240.6 | -5.4 |

7) | 276,509 | +285.9 | 163.2 | +259.1 |

8) | 157,613 | +1.4 | 165.7 | +3.6 |

9) | 129,203 | -9.4 | 105.8 | -7.2 |

10) | 108,356 | +205.7 | 72.8 | +231.7 |

Wine

All but two of the top 10 wine brands in this year’s list have seen volume and value declines, which is broadly typical of the category’s on-trade performance.

Brand | Volume (9LC) | % +/- | Value (£m) | % +/- |

1) | 178,518 | -0.9 | 21.1 | -3.4 |

2) | 111,583 | -14.4 | 77.4 | -11.4 |

3) | 101,369 | -3.5 | 13.7 | -2 |

4) | 99,930 | -12.7 | 21.9 | -10.4 |

5) | 97,372 | -1.8 | 12 | -0.1 |

6) | 91,409 | -10 | 11.4 | -5.9 |

7) | 78,512 | -36.7 | 8.4 | -37.6 |

8) | 76,520 | +81.2 | 14.7 | +70.7 |

9) | 76,227 | -18.7 | 11.1 | -16.3 |

10) | 72,835 | +16.8 | 5.2 | +18.1 |

Ready-to-drink

It’s a category some snub, but the humble ready-to-drink (RTD) is an important part of on-trade drinks sales, with many brands in growth.

Brand | Volume (HL) | % +/- | Value (£m) | % +/- |

1) | 29,022 | -13.8 | 33.4 | -12 |

2) | 25,731 | -10 | 30.1 | -8.1 |

3) | 19,515 | +7.2 | 21.5 | +14.1 |

4) | 13,429 | -2.4 | 9.2 | -1.3 |

5) | 13,023 | +15.5 | 12.4 | +19.7 |

6) | 7,825 | +1.7 | 7.4 | +8.4 |

7) | 6,801 | -12.1 | 6 | -11.8 |

8) | 4,546 | -24.1 | 23.5 | -23.5 |

9) | 3,602 | +7.3 | 3.6 | +9.1 |

- All data provided by CGA, which looks at the 12 months to 11 August 2018